Reporting - What information should I report on?

Understanding what to report on or how to ensure accuracy is achieved can be difficult. We recommend connecting with your accountant to assist you in this matter. Your accountant can help you to understand which reports will be valuable for your business and which systems to consider implementing. If you don’t have an accountant or don’t have a great one, get in touch with our team today.

Accurate reporting allows you to:

- review and track your progress.

- identify areas of concern so they can be improved.

- make informed decisions.

- forecast.

- budget.

- market effectively.

Finding the right financial management system for you

Just as accuracy is crucial in reporting, so too is the financial management system you use. Great financial software should be able to provide you with key decision assisting reports, that you can use to analyse and direct business performance. While also effectively managing your accounting and revenue.

You will need to start by considering what your company needs the software to do and if the software needs to be able to communicate with other systems or software. Consider features such as:

- functionality.

- usability.

- automation.

- security.

- speed.

- support.

- analytics.

- budget.

- flexibility.

- cloud applications.

- business size.

Allowing time to research the varying financial management systems available is vital, not only will this new software effectively manage your revenue, but integrating new software will require a lot of time and resources, so it isn’t something to rush.

Take your time to:

- talk it through with your accountant.

- request demos of how various software works.

- talk to the software account management team, can they clearly outline the features of the software? Is product training available? Is there a helpdesk available and what hours are they in operation?

- talk to others in your network using the same or similar software, and ask them about the limitations that frustrate them, and the features they think are advantageous.

With so many options available, we have suggested you make talking with your accountant your first step. Your accountant should know your business inside and out and should be able to assist you to get the best system to suit your business’s needs. If you don’t have an accountant already or would like a second opinion, please get in touch with our friendly team.

What financial records do I have to hold on to? And, for how long?

No matter the size of your business, if you are self-employed, or a contractor, it is a requirement of the Inland Revenue Department (IRD) that you (not your accountant or bookkeeper, but you the business owner) hold on to all tax records for a minimum of seven years, no matter whether they are paper or electronic based. If you are audited by the IRD you will need to be able to pass all records over to the IRD.

Records you may need to keep include:

- receipts.

- invoices.

- banking records.

- wage books.

- asset registers and depreciation schedules.

- vehicle logbooks.

- petty cash.

- emails of a financial nature, for example, an email that proves a claim was a legitimate business expense, such as organising a business meeting in which flights are required.

- copies of information sent to IRD – this can be managed using MyIR.

- hold onto any calculations you have completed to file your tax return.

- if you are GST registered, you will need to keep all tax invoices for your expenses, so you are able to claim the GST back and can prove their legitimacy as a valid expense

Accounting tip:

To keep on top of your records it is a good idea to record:

- what was purchased.

- by whom.

- the date the purchase was made.

- the reason for the purchase.

- the cost of the purchase.

- the supplier.

Accounting systems like Xero make this very easy to do, even while on the run, allowing you to upload the proof of purchase (receipt) to an expense report with all of the aforementioned detail on your mobile phone.

Assigning an owner to manage the financial records

Choosing the right person, or company to manage your financial records is essential. They must be trustworthy, proactive, and have the financial acumen to deliver and analyse accurate results for the company.

The key tasks a financial manager should be able to complete are:

- produce accurate financial reports.

- reporting analysation, monitoring for noteworthy changes and trends that could impact the business.

- financial advice - clearly communicating their insights to assist you in making financial decisions.

- financial forecasting including projecting the company’s expected profit or loss.

- budgeting.

- managing the business's cash flow and credit.

- directing investments.

Many businesses will partner with an external party to ensure they are getting the best advice for their business. If this is something you would like to investigate, please feel free to reach out to our friendly team of accountants who can assist you.

What is a Trend Analysis?

A trend analysis explains the process of viewing your financials across multiple (with a minimum of two) accounting periods, to understand trends.

Trend analysis can be used with an income statement or a balance sheet and can be completed using absolute comparisons or percentage comparisons. In a percentage comparison, you set a baseline year as 100%. The other years you are comparing are then shown as a percentage above or under what was achieved in the baseline year.

Undertaking regular trend analyses allows you to easily spot trends and growth patterns.

Accounting tip:

The more years of data you compare, the easier it will be to spot trends.

What’s the difference between Horizontal and Vertical Trend Analysis

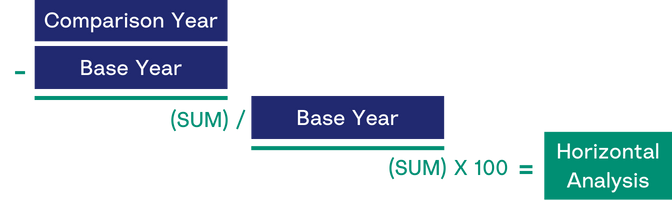

Horizontal Analysis

When completing a horizontal trend analysis, you review changes line-by-line, comparing specific accounting periods (monthly, quarterly, or annually) across at least two years.

For example, if you compare your business's income statement for 2021 and 2022, horizontal analysis allows you to compare the revenue totals for both 2021 and 2022, to see if it changed (increased or decreased) or remained steady.

Horizontal Analysis Formula = {(Comparison Year Amount - Base Year Amount) / Base Year Amount} X 100

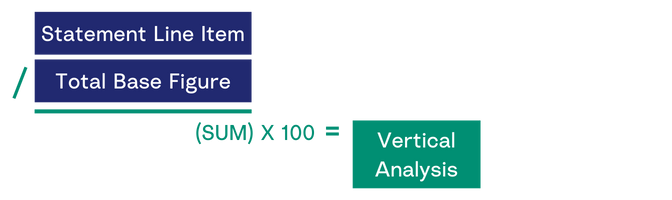

Vertical Analysis

When completing a vertical analysis, you are looking at the percentage of a line item compared to the whole. For example, all line items on an income statement are expressed as a percentage of the gross sales. To explain this further, if you have a trend analysis that shows 35% of the cost of goods sold were made up by sales (the costs involved in selling the product) in 2021, 34% in 2020 and 35% in 2019 then a percentage of 47% in 2022 would be a major concern, as the cost involved in selling your item has drastically increased.

Vertical Analysis Formula = (Statement line Item / Total Base Figure) X 100

Being able to view your sales, assets, and liabilities vertically allows you to determine how your business is performing year on year and allows you to understand which parts of the whole are causing changes either positively or negatively.

How do I analyse my balance sheet?

A balance sheet is basically a snapshot of your business's worth. Also known as a ‘statement of financial position’, it provides detail on your business’ assets, liabilities, and the net worth of the owner/operator.

The balance sheet is split into three sections, Assets, Liabilities, and Owner Equity.

As shown in the following formula, the total liabilities of the business, combined with the owner/operator’s equity, should equal the total assets of the business.

Balance sheet formula: Assets = Liabilities + Owner/Operators Equity

For example, you decide to purchase a tractor for $65,000 (asset) and you do so by borrowing $60,000 from the bank (liability) and using $5,000 of your savings (owner equity). The asset ($65,000) = the liability ($60,000) + owner equity ($5,000).

What is an Asset?

An asset is something that could generate cash flow. Assets can be split into two types, current and noncurrent assets.

Current assets

Current assets represent the total value of all assets that will be/can be expected to be converted to cash within a year. Examples of current assets are:

- cash or cash equivalents.

- stock or inventory.

- accounts receivable (money due for goods or services delivered or used but not yet paid for by the customer).

- prepaid expenses (payments you made in advance of receiving goods or services).

- marketable securities (assets that can be liquidated to cash quickly).

Noncurrent assets

Noncurrent assets represent a company’s long-term investments, or any asset not classified as current. Examples of noncurrent assets include:

- land.

- property.

- equipment.

- long-term investments.

- cash surrender value of life insurance.

- goodwill.

- trademarks

What is a Liability?

A liability is something a person or a business owes. For example:

- bank loans.

- unpaid bills.

- accounts payable (payments you owe your suppliers).

- salaries and wages.

- taxes.

- mortgages.

What is equity?

Equity accounts for the sum of money a business owner has put into their business or what they own after liabilities have been removed.

For example, say you purchased the property that your business resides in for $650,000 in 2012, using a bank loan of $300,000, and $350,000 of your own savings. By 2022 you had paid $150,000 off the principal of your loan (leaving $150,000 to go + interest), and the value of the property had increased to $850,000. In this example, your equity in the property is $500,000.

Asset = $850,000

Liability = $150,000 (the remaining loan owed)

Equity: $350,000 (initial payment for property) + $150,000 (loan paid off) + $200,000 (gains in valuation) = $700,000

How do I analyse my cash flow Statement?

A cash flow statement shows you which parts of your business generated cash and which parts spent cash within a given period.

Within your cash flow statement, there are three sections that you should track:

-

Cash flow from operations (CFO)

Shows the amount of cash coming in from your business’s regular business activities such as goods or services sold, wages paid, income tax, interest payments, payments to suppliers, etc.

-

Cash flow from investments (CFI)

Shows the flow of cash that is being used to purchase, or sell, long terms assets. For example, purchasing/selling investments such as stocks, purchasing/selling fixed assets such as property or equipment, collection of loans, etc.

-

Cash flow from financing (CFF)

This section provides insight into the financial strength of the company as it shows the flow of cash that is used to fund a company, specifically related to raising capital. For example, cash from a loan, interest payments on that loan, repurchase or sale of stock, etc.

Completing a cash flow analysis, allows you to see how much money is available to run operations within your business. An easy way to do this is to complete a Quick Ratio.

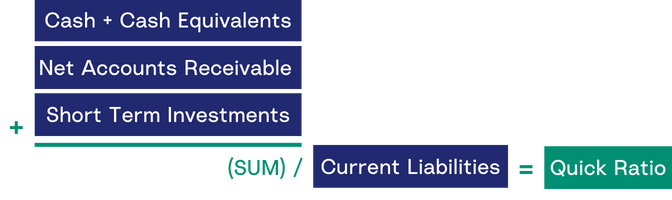

Quick Ratio

A quick ratio shows whether a company can meet its current or short-term obligations based on the dollar amount of its available liquid assets (assets that can be turned into cash in a short amount of time).

The most common way to complete a quick ratio is to add up the business's most liquid assets (cash + cash equivalents, net accounts receivable (money owed to the business for goods or services sold) and divide the total by the business's current liabilities.

If your ratio is greater than 1 it means you are able to meet your current obligations.

How well is your business managing payables and receivables?

To ensure your cash flow stays in a healthy state, it is vital to carefully manage your accounts payable (bills your company needs to pay, excluding payroll) and your accounts receivable (incoming payments for services delivered).

Where possible you want to be paid for your services/products as quickly as possible and delay paying your accounts payable for as long as you can (without incurring late payment fees/ interest). This way you ensure you have access to ample cash in case of unexpected events, such as a piece of machinery needing to be replaced.

Many businesses struggle to get their account receivable process streamlined. Often it comes down to the work flow processes for the business not being as slick as it could be. Processing invoices at the end of the week/month instead of as they are completed is often the culprit and is a process that can very easily be rectified with various software services and technologies that are available today.

How do I calculate the gross profit margin?

The gross profit margin measures the sum of money left over from the sale of your goods or services, once the expenses (to deliver the good or service) are deducted.

Examples of costs of goods and services include:

- materials.

- labour.

- freight.

- production expenses, such as equipment and utilities.

To begin you will need to calculate the gross profit of a product or service, this can be calculated as:

Gross profit = Total Revenue – Cost of Goods Sold (COGS)

To calculate the gross profit margin, you follow this calculation:

Gross Profit Margin = Gross Profit / Total Revenue x 100

Here’s an example of this formula in action, you make and sell children’s bibs. 1 bib costs $5 to make and you sell them for $8.50 each. Your gross profit is $3.50, and your gross profit margin is 41.17%.

Total revenue = $8.50

Total production costs = $5.00

Gross profit: $8.50 - $5.00 = $3.50

Gross profit margin: $3.50 / $8.50 x 100 = 41.17%

Getting your financial reporting and management right is vital. Many of the business owners we work with, got into business because they were good at what they do, and they have a passion for delivering their goods or services to their consumers.

Often their strengths lie in non-financially based business operations, which are equally vital to their business’s success. They often understand the financials very well and know the vital importance of them, but they also know their knowledge is limited. However, they know that doesn’t matter because a great business owner knows to play to their strengths. They understand the value of delegating tasks to ensure they are managed optimally by either internal or external parties.

If you would like assistance in managing your financials to optimise your business, or would simply like to ensure you are compliant and are getting the most out of your business’s operations get in touch with the friendly team at RightWay.

In this article, we dig into provisional tax and ways to manage your tax to ease the burden on your cash flow. We'll cover off what provisional tax is, working out your provisional tax payments, payment options, due dates and so much more!

We’ve all heard of GST, (short for “Goods and Services Tax”) as we’ve had to pay it! It’s that annoying tax that makes goods and services more expensive right?

But what about if you are the person selling the goods or service? GST from this angle is far less understood and can be far more complicated.

In this blog, we are going to dive into all things GST answering all those nitty-gritty questions, including, when you should register for GST, the rules around filing your returns, and which accounting basis could be right for you...

Paying tax is a fact of life for anyone earning a living - businesses included. In this article, we discuss some of the aspects of tax compliance that you should be aware of as a business owner, including PAYE, Business Income Tax, business expenses, GST, balance dates, Kiwisaver, student loans, and actually paying